Entrepreneurs are the seeds to great protocols, VCs are the fertilizers that aid in its growth using which the entrepreneurs grow the entire tree — so users can enjoy the fruits it bears.

That is in essence what any VC to any industry is — a gardener. It’s a purely symbiotic relationship — and a most essential one. Within crypto, we have seen this relationship reach new heights as there has been an influx of capital to various protocols and startups. To crunch some numbers, the industry has seen over $27B invested just as of November. This amount is mind-numbing. But so is the number of protocols that have emerged.

Venture capital has always been at the forefront of innovation — where the money goes, innovation grows. But could it be that innovation is being indirectly controlled by these funds? It was reported that over $400M worth of DeFi deals were declined between the second and third quarter of 2021. Does this stop protocols from growing?

These questions are unsettling. But their answers aren’t.

In this Magnify, I aim to explore the apparent innovation centralization by investment funds, the rise of Venture DAOs to counteract that, and why all of it is closely tied with the growth of the industry.

Let’s dive in.

If I’m in, I’m all in

That is a cheesy line I picked up from one of Hugh Jackman’s hilarious marketing videos for RM Williams. If you’ve watched the ad then you’d know what I intend to talk about here.

Crypto may be a labyrinth, but it is one where it is worth spending time getting lost in. Most VCs upon entering the space see a plethora of opportunities. From trading/brokerage firms to service providers in DeFi — there is a sea of protocols that a big-pocketed investor can favor. But where must they begin?

The first option is to get into the market earlier than most others. That is how Andreessen Horowitz entered the crypto space back in 2013 when they invested about $20M in Coinbase. Today, a) Coinbase is a publicly-traded company on the NASDAQ and b) is one of the most active crypto investment firms under its investment arm Coinbase Ventures.

The second option is to carefully examine the industry from a researcher’s standpoint and use previous experience to invest in truly disruptive companies. That was Paradigm’s approach when it was first launched. Fred Ersham’s experience as the Coinbase co-founder combined with Matt Huang’s knowledge of the industry (from his exposure to crypto at Sequoia Capital) was the perfect seed for an investment arm to grow. And the results of this combination have bore fruit — recently, the firm announced an additional $2.5B crypto fund.

The third option is to follow suit of these investors who have stood the test of time. Some of the biggest hedge funds (and even some pension funds) are now entering the space that is offering (or are planning to offer) direct crypto exposure to their clients.

Ryan Selkis sums this up perfectly when he says that VCs “move in and down but not out”. Despite all the irrational behavior of crypto markets this year, the industry has been flushed with over $6B from various VCs — in Q3 alone.

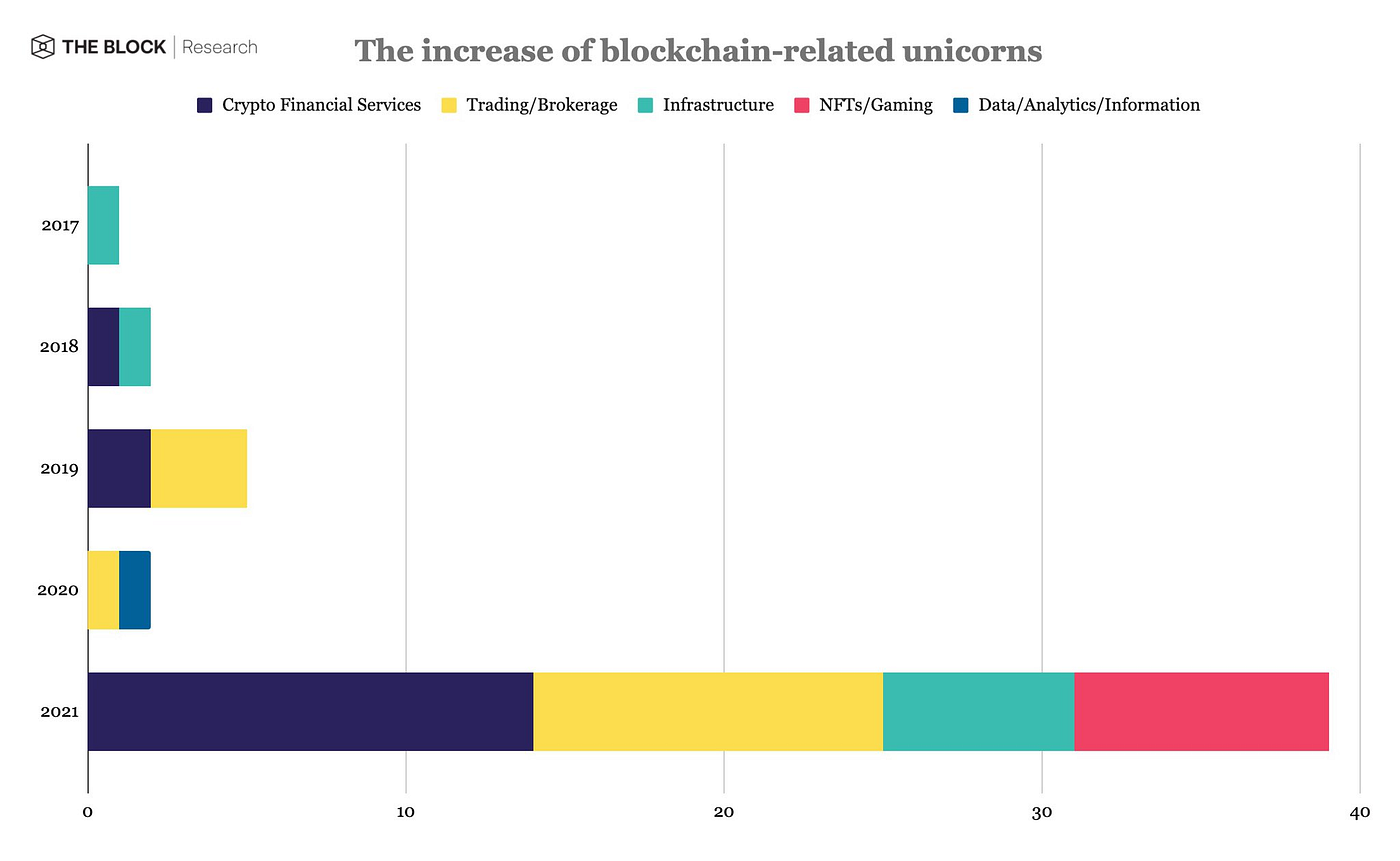

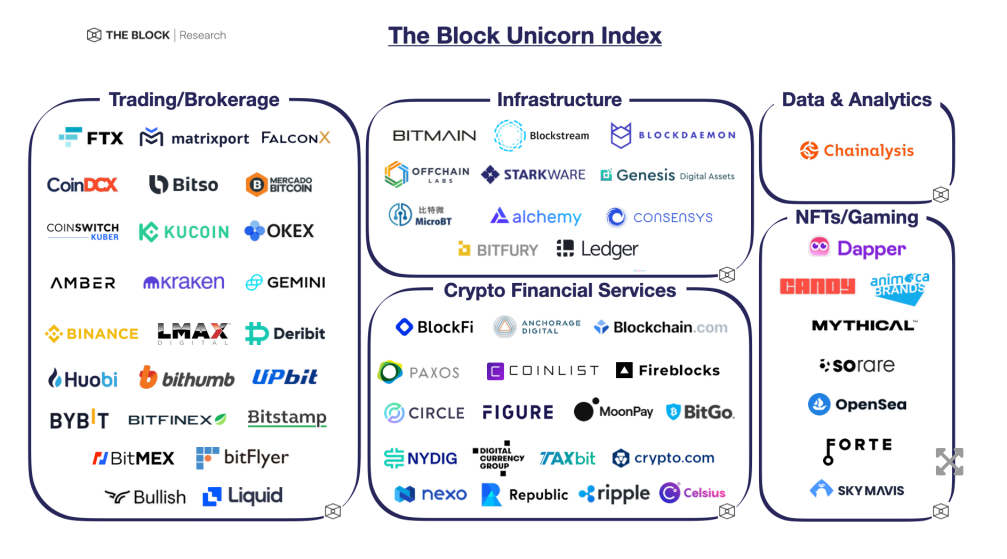

Slightly relaxed regulations, reluctance to erect an outright ban and the larger acceptance of the industry have fueled this inflow of cash. All of this has resulted in the emergence of major unicorns within the industry. The Block Research’s Unicorn Index reveals that over 60 crypto unicorns have emerged just this year — dwarfing the number from all previous years.

A number of these crypto protocols have had 1,850% YoY across a wide spectrum of the industry.

However, this still all leaves us with a pertinent question — who is driving the innovation in crypto? Do VCs decide which protocol takes precedence over the other? And even if they do, can something like Venture DAOs combat that?

VentureDAOs — Breaking the vulture culture?

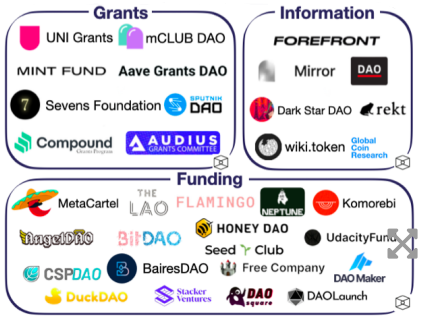

Venture DAOs are the new frontier of venture capital. They consist of two major components: a) an on-chain one that manages the operations and b) an off-chain component that manages the legal framework for the fund. Compared to a VC, there are two benefits that a Venture DAO provides:

- Community-driven membership — each member is an investor and can source and propose projects for investment

- Investment decisions are made subject to the DAO voting results (some even support quadratic voting)

The critical legal aspect of DAOs is often managed by a parent LLC. The perfect example of this is The LAO, which is based in the United States and is a Delaware LLC. It has funded over 30 projects since its inception in April 2020. The legal logistics and paperwork are often handled by a service provider. Stacker Ventures, for instance, is an open protocol without any legal status as a corporation.

But even the biggest DAOs within the ecosystem are tied to major VCs in the back. For instance, Uniswap, Compound, and Maker have had substantial investments coming in from Andreessen Horowitz. BitDAO — a “decentrally-governed” treasury that aims to support emerging projects in DeFi — is being backed by huge investors like Peter Thiel, Pantera, Dragonfly Capital, and more.

And these are just some examples — the network of VCs backing the entire crypto industry has only been increasing. But this doesn’t undermine the core structure of the Venture DAOs — an institutional investor with a seven-figure investment is similar to one with a five-figure investment. Granted, however, that in some cases the higher the investment the greater the influence over the DAO itself.

That said, there are certain challenges that mustn’t be looked over. A company might find it hard to share its confidential information with all the DAO members — some of them could have an affiliation with a competitor. Furthermore, giving allocation to a Venture DAO (with 100s, if not 1000s) of members is even more difficult — members have a disparate contribution. This would mean allocation would need to be such as well.

So, where do we go from all of this?

VCs as Catalysts

For the everyday investor/trader who is looking at a bunch of companies to add to their portfolio, a VC can act as a stamp of approval. And why not? Most firms have analysts that help drive crucial investment decisions only after analyzing whether the company has a product-market-fit, among several other factors. Coming back to the original question…do VCs then influence innovation? Yes, they do. But isn’t that what we eventually want?

Don’t we want the industry to proliferate as deeply as possible? If VCs help pump money to protocols that have an incredible solution to a critical problem — then on what grounds is it not innovation? Also, crypto is a purely capitalist environment. Everything depends on the product and the community that uses it. A VC can back the best-looking protocols on the planet but if it doesn’t serve the community well, then they are bound to face the heat.

In addition to driving innovation, VCs also help cement the community’s faith in the industry. If the “smart” money is moving in consistently, then surely something must be right within the industry too.

Whether it's Venture DAO or Venture Capital, we must understand that they are merely catalysts. At the end of the day, it is the core team of the protocol that makes the magic happen. They are the ones who are putting in all the effort to iron out every minute detail and ensure that the product fulfills its objectives. In our discussions around VC (or even Venture DAO), we mustn’t forget that they should complement the entire life-cycle of the protocol

Like the above article 👆? I uncover one intricate topic each week and share my thoughts. I’m @mohakagr on Twitter.

About ClayStack:

ClayStack is a decentralized cross-chain liquid staking protocol backed by leading funds and angels including CoinFund, ParaFi, and Coinbase Ventures. At its core, the platform helps users effortlessly stake their crypto assets while maintaining their liquidity.

Get the latest updates!

Learn more about ClayStack, interact with our team, engage in community discussions, and share your valuable feedback.

- Telegram: https://t.me/claystack

- Twitter: https://twitter.com/ClayStack_HQ

- Website: https://claystack.com/

- Announcements: https://t.me/claystackchannel

- Discord: https://discord.gg/yCDV2CgZMb